myVPZ

Languages

One of the most common and simultaneously important questions in retirement planning is: Should I take my pension fund savings as an annuity, a lump sum, or a combination of both?

Which option is best for you depends on various factors—including your financial situation, life plans, as well as tax and family considerations. Unfortunately, in practice, many people make this decision too late or without sufficient information. Once made, it is final and hardly reversible.

The decision to take a lump sum, an annuity, or a combination requires a careful, professional, and early analysis. Key influencing factors include:

- Personal goals and priorities

- Family situation (e.g., providing for dependents)

- Other income sources such as AHV or private pensions

- Existing assets and budget

- Health status and life expectancy

- Tax implications

- Regulations of your pension fund

Depending on the regulations, various payout options are possible. By law, a lump-sum withdrawal of at least 25 % is guaranteed. Many pension funds also allow higher lump-sum proportions or combinations of annuity and lump sum.

Important: A lump-sum withdrawal must be requested within the required timeframe, usually one to three years before retirement. The exact deadlines can be found in your pension fund regulations. The decision is binding and final.

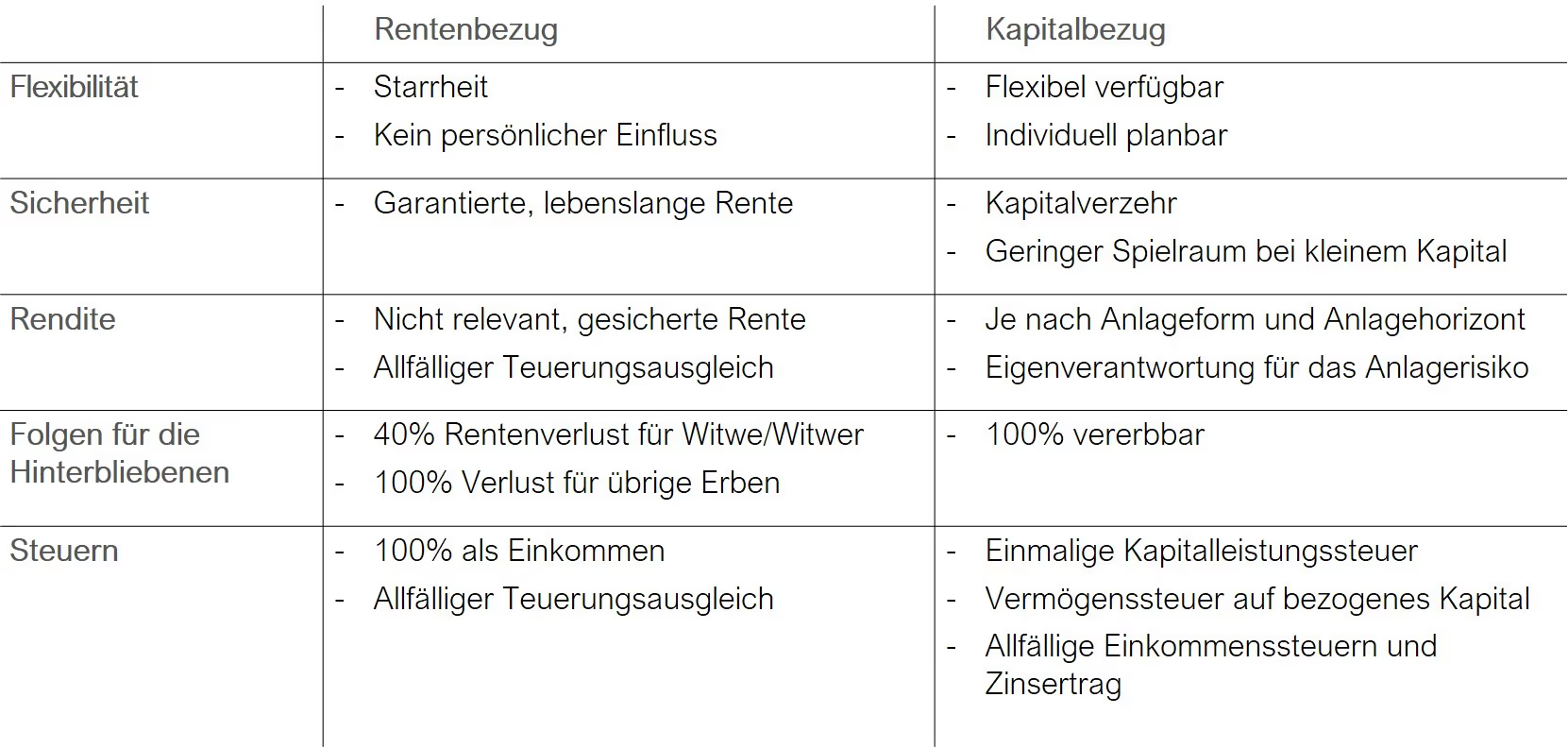

Advantages of an annuity

- Lifetime payments – regardless of how long you live

- Planning security with regular expenses

- No investment risks – responsibility lies with the pension fund

- Spousal protection in the event of death (60 % widow’s/widower’s pension, depending on BVG regulations)

Disadvantages of an annuity

- No access to the capital anymore

- 100 % taxable as income from the start of pension payments

- Remaining capital is not inheritable

- Inflation protection is not guaranteed – depends on the financial situation of the pension fund

- No widower’s pension if the wife dies first and was receiving a pension (depending on BVG revisions)

Advantages of a lump-sum withdrawal

- Free access to the capital for investments, home ownership, mortgage repayment, or larger personal goals

- Inheritable by spouse, partner, children, or any other designated beneficiaries

- Flexibility in asset management (return opportunities, risk profile, liquidity planning)

- Tax optimization possible through staggered withdrawals (e.g., over several years and accounts)

Disadvantages of a lump-sum withdrawal

- Personal responsibility for managing, investing, and using the capital

- Lifetime financial security must be planned independently

- Investment and inflation risks are borne by you

The choice between a lump sum and an annuity is highly individual. No guidebook or online calculator can fully reflect your personal situation. What matters most are your life goals, financial situation, and need for security. Early, independent advice ensures that you make a well-informed and sustainable decision—protecting your financial security and quality of life in retirement.

For an initial, free, and non-binding informational consultation, please contact us by email at kontaktanfrage@vpz.ch or call our free VPZ hotline at 0800 822 288 to schedule an appointment directly with your advisory specialist. Comprehensive planning with foresight coordinates your situation, identifies optimization opportunities, and ensures long-term success.