myVPZ

Languages

A thorough analysis of the private pension situation often reveals a sobering picture: without targeted wealth accumulation for retirement and without individually tailored risk protection in case of disability due to accident or illness, or in the event of death, significant financial risks exist.

Many people do not know the exact status of their retirement provision, today or in the future. Private pension planning is a complex and often emotionally charged topic for many. There is frequently the misleading belief that in Switzerland, one is automatically sufficiently covered. However, this is rarely the case. The reality is often quite different.

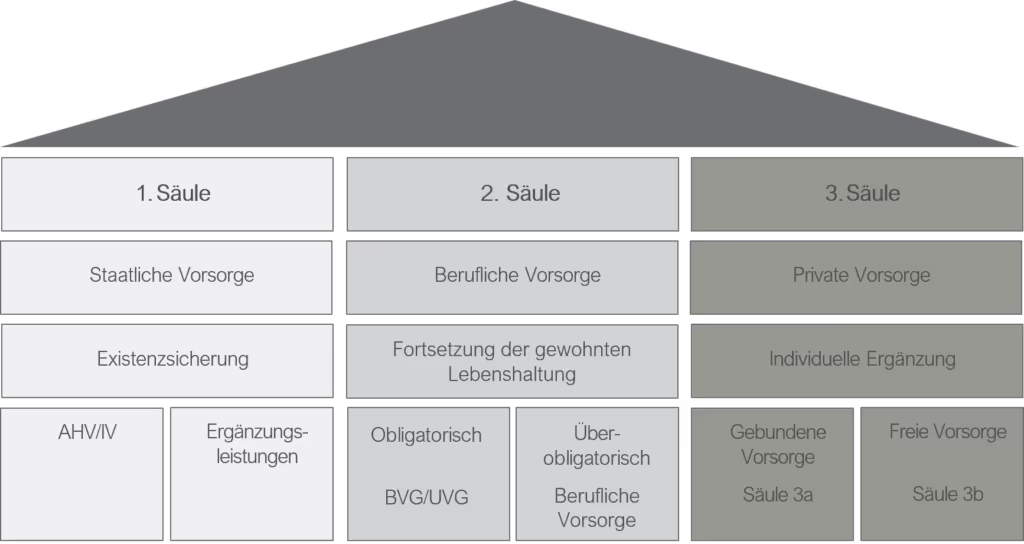

Our three-pillar pension system is complex. Legal requirements are constantly changing, and the offerings from banks and insurance companies are difficult to compare. A professional and independent analysis helps with this:

- Identify existing benefit gaps

- Assess risks realistically

- Develop meaningful solutions tailored to your personal situation

Especially in the event of disability, death, or retirement, the benefits from Pillars 1 and 2 are usually insufficient to maintain the accustomed standard of living. Therefore, it is crucial to build and strategically strengthen private pension provision (Pillar 3) at an early stage.

- Contribute the maximum annual amount to Pillar 3a (from 2025: CHF 7,258 for employees with a pension fund / CHF 36,288 for employees without a pension fund)

- Use a securities solution to achieve higher long-term returns than with a traditional savings account

- Compare the terms of different providers (fees, products, investment strategies, flexibility)

- Open multiple Pillar 3a accounts to stagger withdrawals at retirement, optimizing taxes

- Avoid withdrawing Pillar 3a funds in the same year as pension fund or vested benefits to reduce tax progression

- Contributions may still make sense after retirement if you continue working

- Employed persons can withdraw their 3a balance no earlier than 5 years before and no later than 5 years after reaching the standard retirement age

- Non-employed persons must withdraw their balance no later than the standard retirement age

For an initial, free, and non-binding informational consultation, please contact us by email at kontaktanfrage@vpz.ch or call our free VPZ hotline at 0800 822 288 to schedule an appointment directly with your advisory specialist. Comprehensive planning with foresight coordinates your situation, identifies optimization opportunities, and ensures long-term success.