myVPZ

Languages

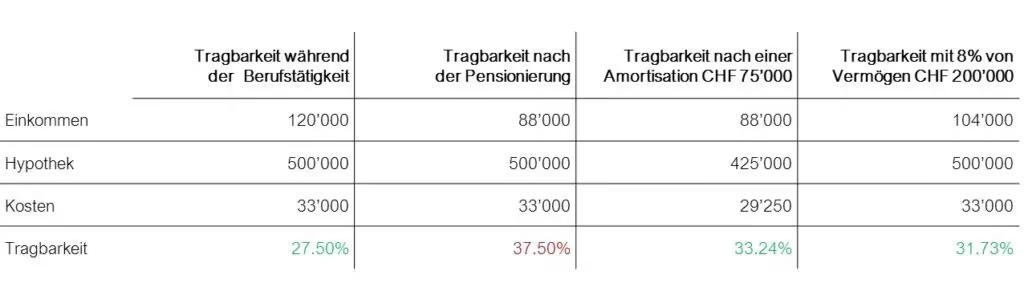

Upon retirement, income often decreases significantly, while fixed costs for homeownership usually remain constant. This raises the crucial question: Will your mortgage remain affordable in retirement?

According to many financial institutions, ongoing fixed costs—including interest, potential amortization, and ancillary expenses—should not exceed one-third of your income after retirement. This is calculated using an interest rate of up to 5 %. Early planning and targeted preparation are therefore essential.

Income in Retirement

After retirement, income typically drops to around 60–70 % of previous earned income. It generally consists of the following sources:

- AHV pension

- Occupational pension plan (BVG / 2nd pillar)

- Private savings (3rd pillar or other assets)

Private savings are a key lever: the earlier you start building them, the higher your future benefits.

Calculating Costs

Despite historically low interest rates, many financial institutions still calculate using a hypothetical interest rate of up to 5 %. Additional costs for the property, such as maintenance and utilities, are often estimated at 1 % of the property’s market value per year. This calculation method can lead to cash flow bottlenecks in retirement.

Available Options

1. Increase income

- Make additional contributions to your occupational pension (2nd pillar), if possible

- Build up and strategically use your 3rd pillar savings

- Generate additional income, e.g., by renting out part of your property

2. Reduce costs

- (Partial) amortization of the mortgage to reduce interest burden

- Avoid taking out a 2nd mortgage (if financing is in two stages)

- Compare financing offers for more favorable terms

3. Leverage assets

- Liquidity can be included in affordability calculations. Many banks assume an annual return of 4–8 %, which for assets of CHF 200,000 corresponds to an income of CHF 8,000–16,000.

If it still becomes tight

If the home remains unaffordable despite all optimizations, further options should be considered:

- Moving to a more affordable housing solution

- Selling the property

- Early transfer of ownership to the next generation

For a first, free, and non-binding informational consultation, you can contact us by email at kontaktanfrage@vpz.ch or call our free VPZ hotline at 0800 822 288 to schedule a direct appointment with one of our advisory specialists. A comprehensive, forward-looking plan coordinates your situation, identifies optimization opportunities, and ensures long-term success.